All Categories

Featured

Table of Contents

Dividend options in the context of life insurance coverage refer to just how insurance policy holders can select to make use of the dividends produced by their entire life insurance coverage plans. Which is the oldest life insurance coverage firm in Canada, has actually not missed a returns settlement because they first developed an entire life plan in the 1830's before Canada was even a country!

This is just recommended in case where the survivor benefit is very vital to the policy proprietor. The added expense of insurance coverage for the improved protection will reduce the cash money value, therefore not suitable under infinite financial where money worth determines exactly how much one can borrow. It is necessary to note that the schedule of dividend options may differ relying on the insurance provider and the specific policy.

Although there are wonderful advantages for limitless banking, there are some things that you should take into consideration prior to entering into infinite banking. There are also some disadvantages to unlimited financial and it may not be suitable for somebody who is searching for economical term life insurance, or if someone is checking out purchasing life insurance policy only to shield their household in the occasion of their death.

It is necessary to recognize both the advantages and restrictions of this economic technique prior to choosing if it's best for you. Complexity: Infinite financial can be intricate, and it's vital to comprehend the details of exactly how an entire life insurance policy jobs and exactly how policy lendings are structured. It is essential to properly set-up the life insurance policy plan to optimize unlimited financial to its complete possibility.

What is the long-term impact of Wealth Management With Infinite Banking on my financial plan?

This can be especially problematic for individuals that count on the survivor benefit to offer their enjoyed ones (Infinite Banking account setup). On the whole, infinite financial can be a helpful financial approach for those who recognize the information of just how it works and agree to approve the prices and restrictions related to this financial investment

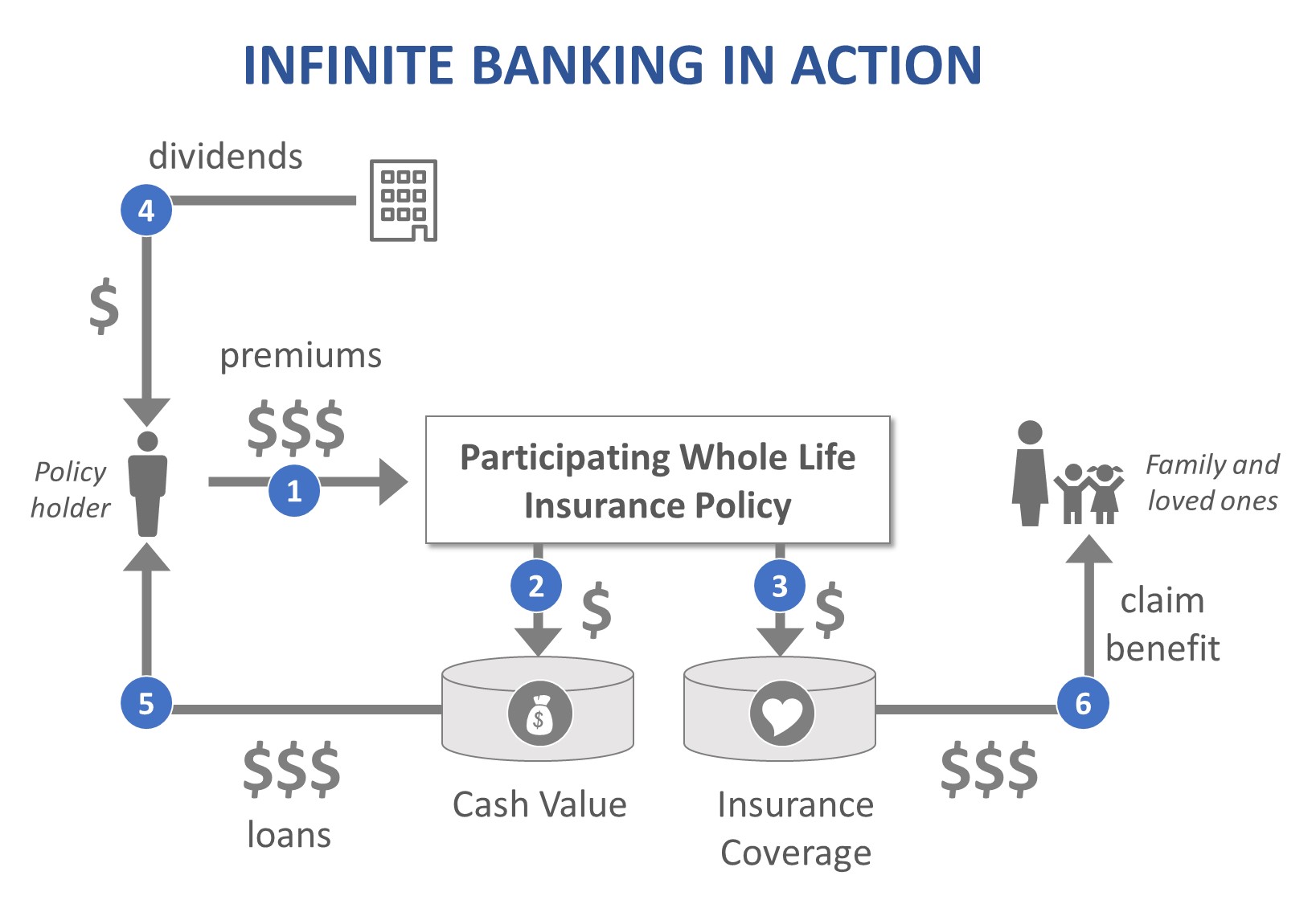

Most business have 2 various types of Whole Life strategies. Over the program of numerous years, you contribute a considerable quantity of money to the policy to construct up the cash money worth.

You're basically offering cash to on your own, and you pay back the car loan gradually, often with passion. As you pay off the car loan, the money value of the plan is renewed, allowing you to borrow versus it once again in the future. Upon fatality, the survivor benefit is minimized by any kind of impressive fundings, yet any remaining survivor benefit is paid tax-free to the beneficiaries.

How do I leverage Leverage Life Insurance to grow my wealth?

Time Perspective Risk: If the policyholder makes a decision to cancel the plan early, the money surrender values might be considerably less than later years of the policy. It is suggested that when exploring this strategy that has a mid to lengthy term time horizon. Taxes: The policyholder might incur tax obligation effects on the financings, dividends, and death benefit payments received from the plan.

Complexity: Limitless banking can be complex, and it is essential to comprehend the details of the policy and the money buildup part before making any kind of financial investment choices. Infinite Financial in Canada is a legit financial approach, not a fraud. Infinite Financial is an idea that was created by Nelson Nash in the United States, and it has given that been adapted and implemented by economic specialists in Canada and other nations.

Policy finances or withdrawals that do not surpass the adjusted cost basis of the plan are taken into consideration to be tax-free. If plan fundings or withdrawals surpass the modified cost basis, the excess amount might be subject to taxes. It is very important to keep in mind that the tax benefits of Infinite Banking might undergo change based on adjustments to tax obligation legislations and guidelines in Canada.

The dangers of Infinite Financial include the possibility for policy finances to minimize the death advantage of the policy and the possibility that the plan might not do as anticipated. Infinite Financial might not be the finest technique for everybody. It is very important to meticulously think about the prices and potential returns of getting involved in an Infinite Financial program, as well as to completely research and understand the affiliated threats.

Is there a way to automate Infinite Banking Vs Traditional Banking transactions?

Infinite Financial is different from traditional financial because it allows the policyholder to be their own source of funding, as opposed to counting on standard financial institutions or loan providers. The insurance policy holder can access the cash worth of the plan and utilize it to finance purchases or investments, without needing to go through a traditional loan provider.

When many people need a car loan, they use for a line of credit history through a conventional bank and pay that financing back, over time, with passion. For physicians and various other high-income income earners, this is possible to do with unlimited banking.

Here's a monetary expert's evaluation of boundless banking and all the pros and cons included. Infinite financial is a personal banking technique developed by R. Nelson Nash. In his publication Becoming Your Own Banker, Nash discusses just how you can utilize an irreversible life insurance policy policy that builds money worth and pays dividends hence releasing yourself from having to obtain money from loan providers and repay high-interest finances.

What is the best way to integrate Financial Leverage With Infinite Banking into my retirement strategy?

And while not every person gets on board with the idea, it has actually challenged hundreds of hundreds of people to rethink exactly how they financial institution and just how they take loans. Between 2000 and 2008, Nash released 6 editions of the book. To this particular day, monetary experts ponder, practice, and discuss the principle of limitless financial.

The unlimited financial idea (or IBC) is a bit more complex than that. The basis of the unlimited financial principle starts with long-term life insurance policy. Limitless banking is not possible with a term life insurance coverage policy; you need to have a long-term money worth life insurance policy. For the concept to function, you'll require among the following: an entire life insurance policy plan a global life insurance policy policy a variable global life insurance policy plan an indexed global life insurance policy If you pay greater than the called for month-to-month costs with permanent life insurance policy, the excess contributions gather cash worth in a money account. Whole life for Infinite Banking.

With a dividend-paying life insurance coverage plan, you can grow your money worth also quicker. Mean you have an irreversible life insurance plan with a shared insurance policy firm.

{kind=link}

Table of Contents

Latest Posts

How To Become Your Own Bank

Infinite Banking Simplified

How To Become My Own Bank

More

Latest Posts

How To Become Your Own Bank

Infinite Banking Simplified

How To Become My Own Bank